BP’s Green Board Disarray

BP's directors are struggling to re-focus the company, likely left vulnerable by a UK governance code adverse to long (steadying) tenure - something Exxon's old guard did not suffer after Engine No. 1

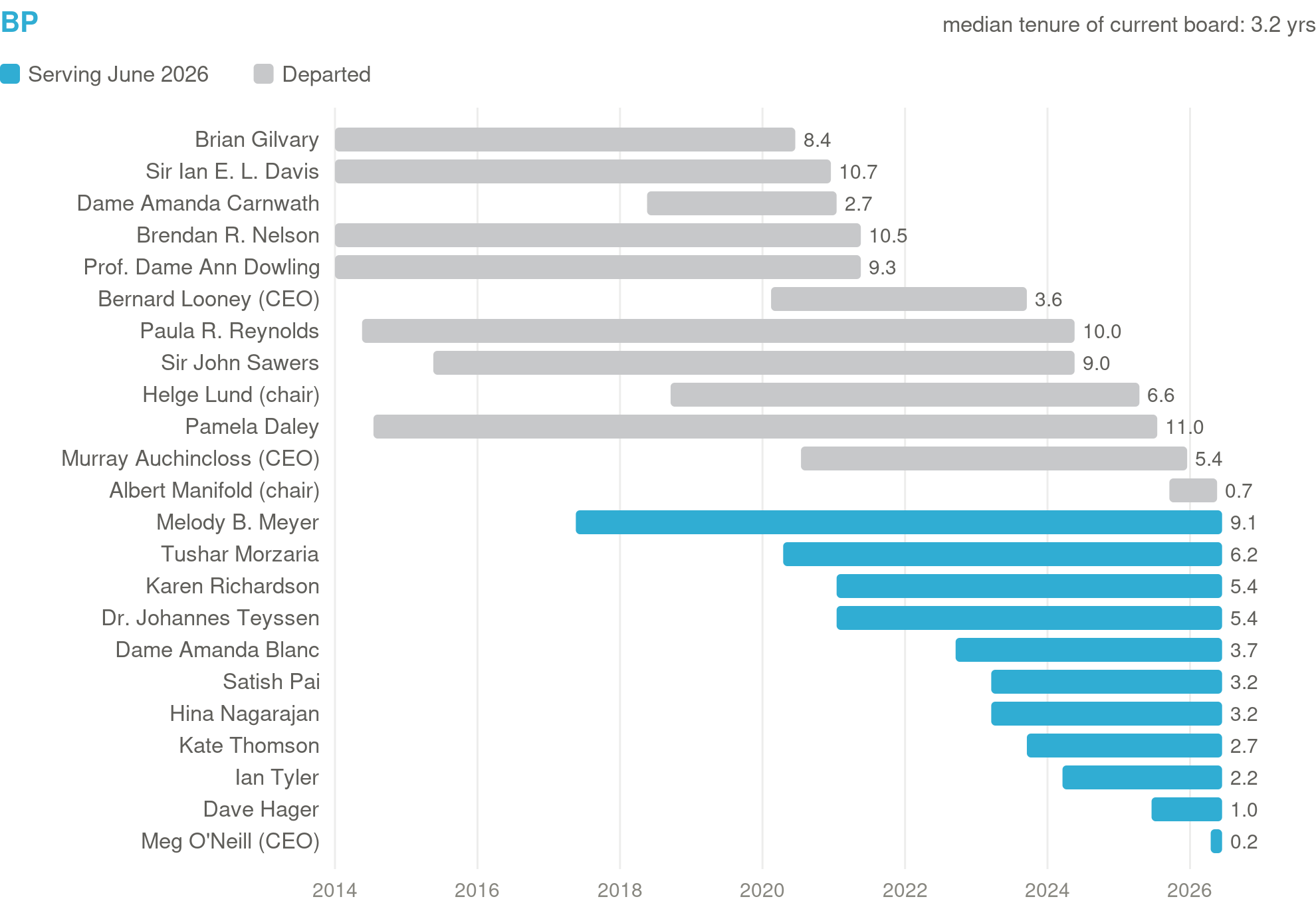

Only one BP director was around before its 2020 low-carbon pivot, and that lack of institutional memory may be playing an important role in its recent leadership turmoil. Two weeks on since BP fired its chairman on May 26 after less than eight months in the job, and less than two months under new CEO Meg O’Neill, investors still seem unsure what happened. Albert Manifold arrived last September, taking the chair in October, with the blessing of activist Elliott Management that had called for the company to get back to petroleum. He was hired, and then fired, by a board with average tenure under four years.

One important reason for the shorter tenure is the U.K. Corporate Governance Code’s nine-year independence clock that encourages companies to shuffle off directors. In the U.S. there are no longevity-based independence rules and companies will routinely have some directors serving over 10 years (sometimes too many).

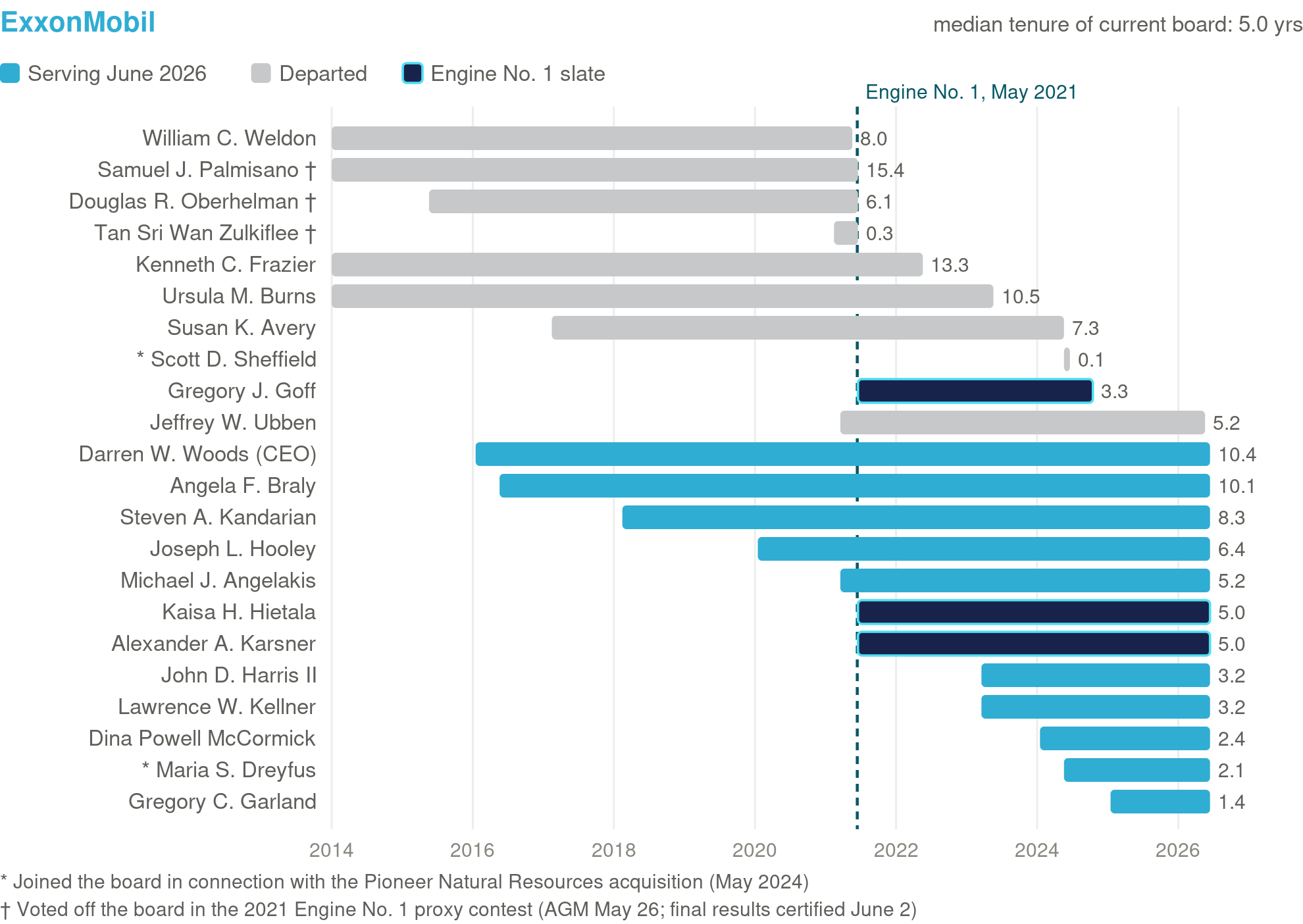

There are many, many reasons ExxonMobil and Chevron have stuck to oil and gas while the European oil majors pivoted away and now pivoting back, but steadier board leadership is potentially one of the factors. A noteworthy comparison is even when Exxon lost three board seats in 2021 to activist Engine No. 1, the new directors were absorbed and the company’s strategy stayed largely unchanged – benefiting its stock performance over the period.

BP’s Pivot and Pivot Again

With a new CEO in February 2020, BP under Bernard Looney unveiled a strategy to embrace a lower carbon energy transition. Shortly after his start and pivot, several directors who were pushing 9 years in service departed. Issues of personal relationships, a CEO change and the reality of a slower, more challenging energy transition saw activist Elliott Management disclose a stake of around 5% in February 2025 and it pressed BP to abandon its energy-transition strategy in favor of oil and gas. Chairman Helge Lund — who had championed that strategy alongside former CEO Bernard Looney — announced his exit within weeks, in April 2025. Albert Manifold, the former CRH chief credited with that company’s value-creation machine joined the board on September 1 and took the chair a month later. In December 2025 the company announced Meg O’Neill, former CEO of Woodside Energy, would become BP’s third CEO (fourth if you count an interim) since 2020. By late May 2026 the board had removed Manifold unanimously and with immediate effect, citing conduct and governance concerns, including reported complaints that he bypassed the board and mishandled sensitive information. Manifold says he was removed “without warning and without explanation.” Ian Tyler, a director since only 2024, is interim chair.

The Nine-Year Independence Clock

A pressure point for BP and all U.K. companies is the Corporate Governance Code treats nine years as the expiry date on a non-executive’s independence: Provision 10 lists service beyond nine years from first election among the circumstances likely to impair independence, and Provision 19 says the chair should not remain beyond nine years from first joining the board. Companies can explain rather than comply. In practice, almost nobody wants to write that essay. The result is visible in BP’s register: Pamela Daley left at 11 years, Paula Reynolds at 10, John Sawers at 9. Today the longest-serving BP director, Melody Meyer, is at 9.1 years — and on the clock.

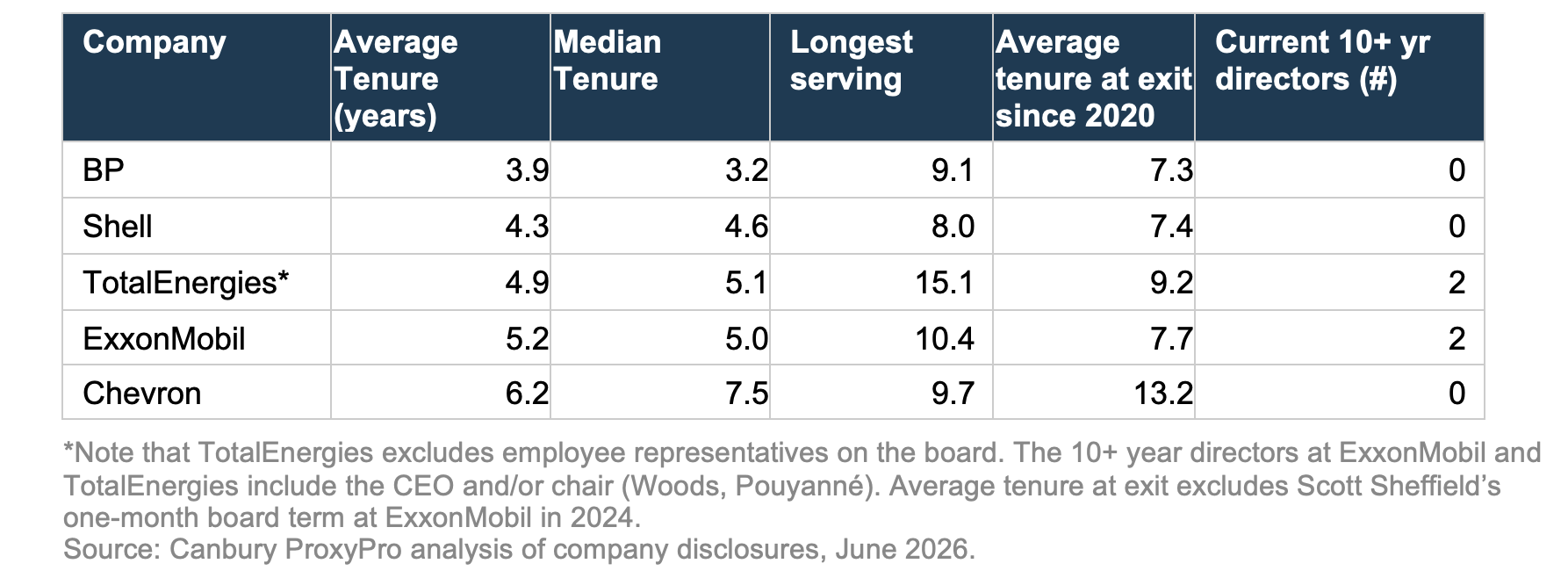

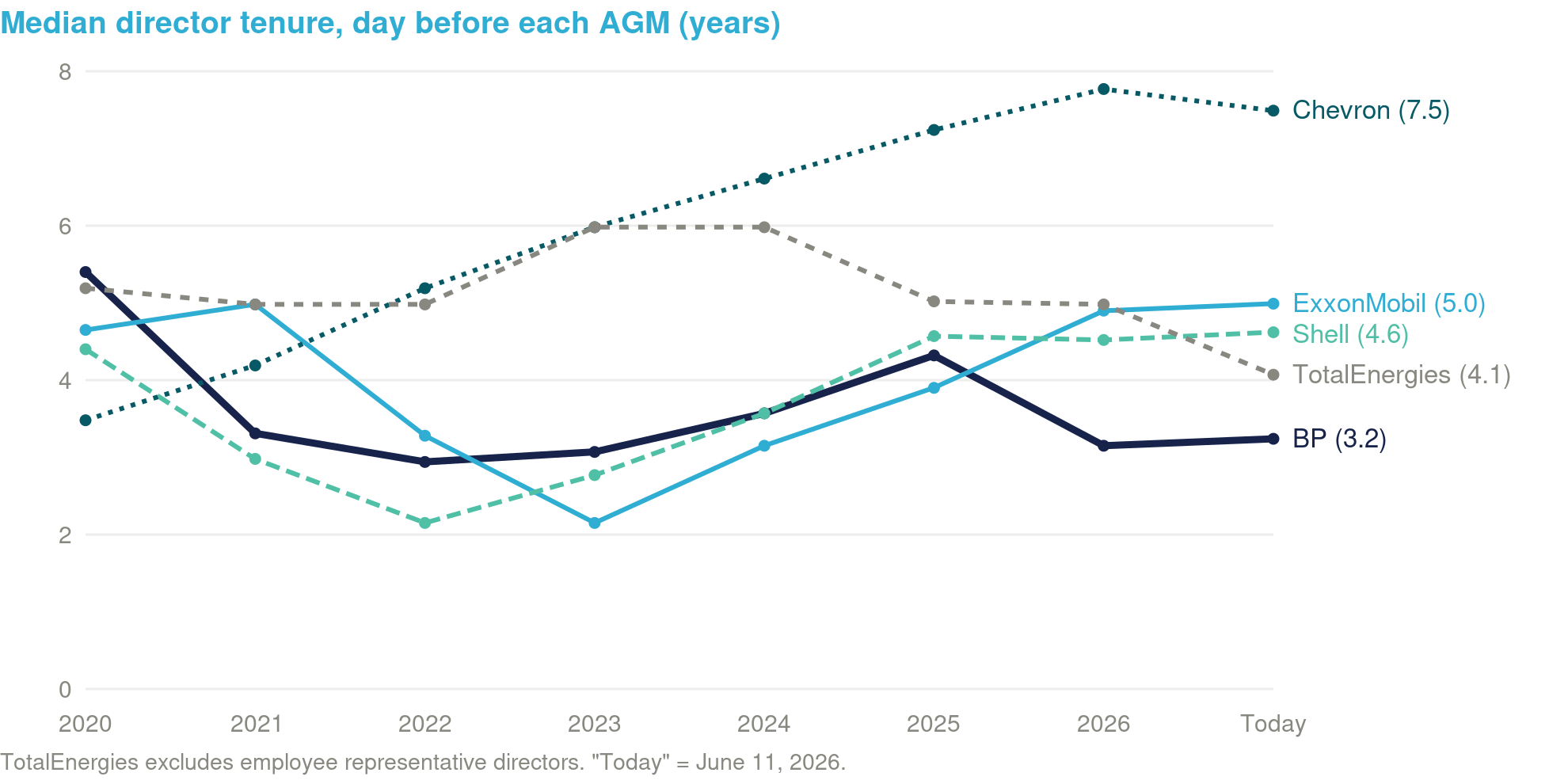

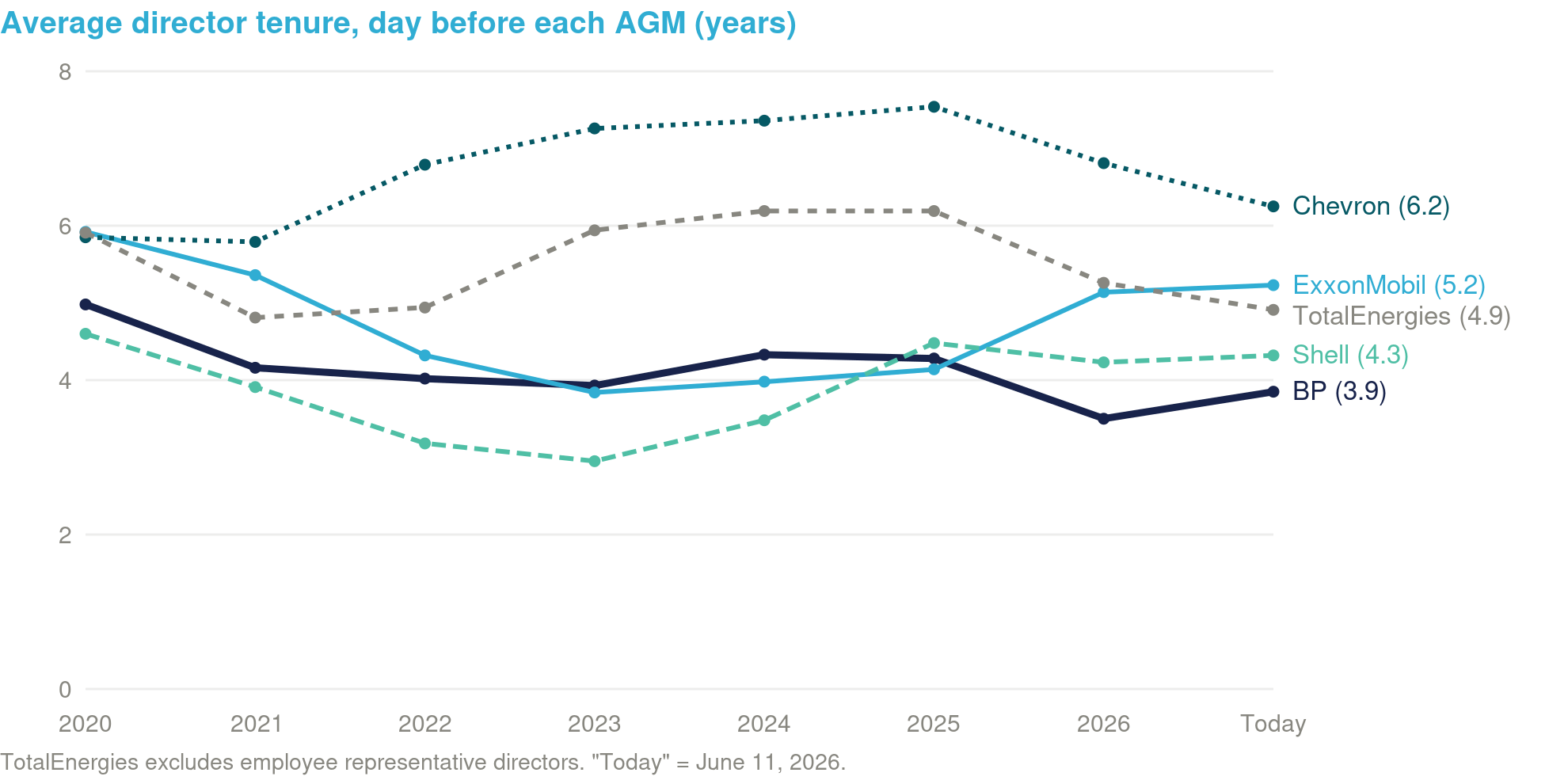

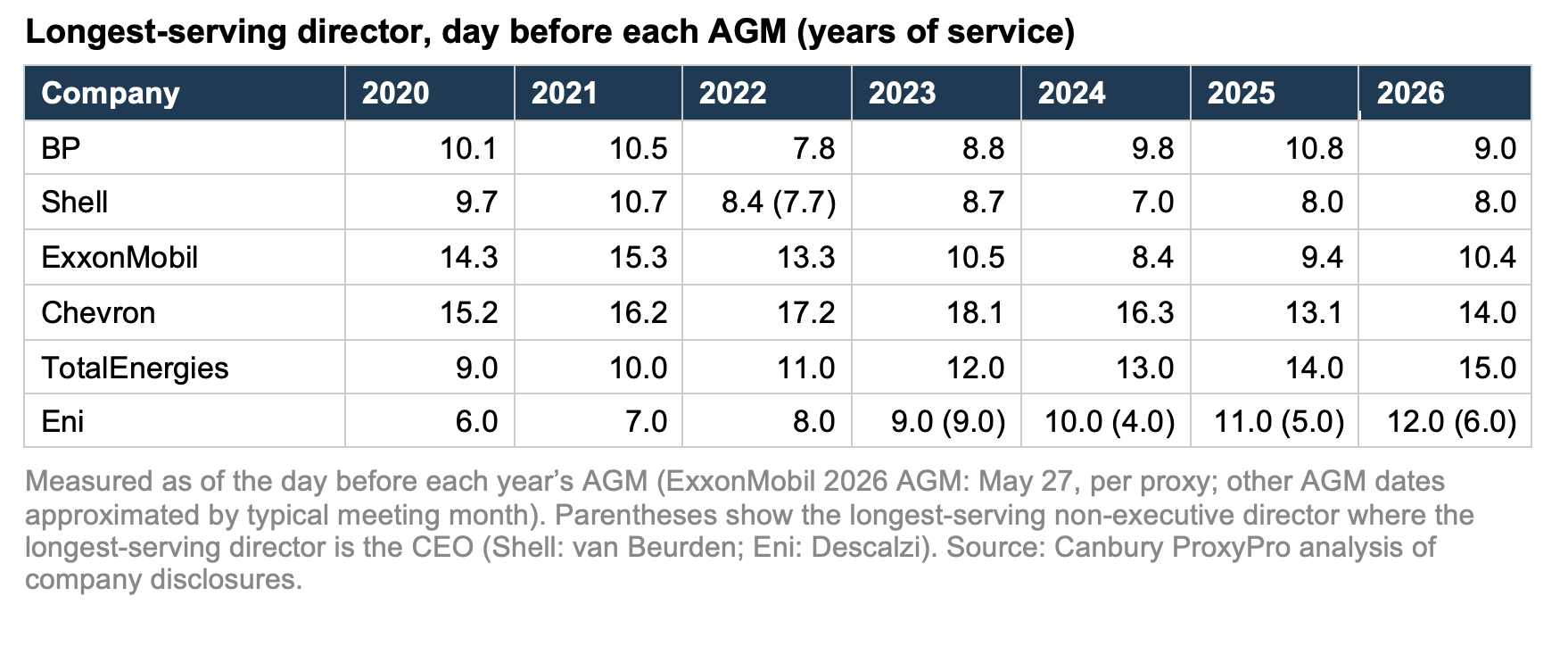

Running the numbers across the six supermajors and the trans-Atlantic, and even trans-Channel difference is apparent. BP’s current board has a median 3.2 years of service with zero directors past ten. Shell, under the same Code, looks nearly identical. Chevron, facing no such convention, has a board averaging 6.2 years and a median 7.5 years; its recently departed directors averaged 13.2 years of service, with one leaving after 18. Exxon’s board, even with turnover following the 2021 proxy contest and new directors as part of its Pioneer Natural Resources acquisition, has the second-longest average tenure at 5.2 years. TotalEnergies, under France’s softer norms, keeps a 15-year veteran as a designated non-independent voice. (Eni is its own governance genre: the Italian state effectively appoints two-thirds of the board and has tenure independence rules. As such, its data has been excluded).

The AGM-by-AGM view sharpens the contrast. Exxon went into the 2021 Engine No. 1 vote with an average director tenure of 5.4 years and two directors past the decade mark. BP's veterans have steadily aged out with four directors departing at around the ten-year mark since 2020. Shell has fielded no 10-year director at an AGM in this period since 2020. Chevron put two to four decade-plus directors before shareholders at every AGM from 2020 through 2025. Exxon’s board tenure dropped noticeably after 2021 when it lost three board seats to Engine No. 1’s nominees, but the seeming tsunami proved but a ripple.

The Exxon Contrast

Exxon offers an intriguing contrast. In May 2021 the company lost a proxy fight to Engine No. 1, a fund holding 0.02% of shares, which placed three directors — Gregory Goff, Kaisa Hietala and Alexander Karsner — on the board over management’s objections. A bruising defeat, on paper, worse than anything Elliott has done to BP, where the activist never even sought a board seat.

Three new directors is not the same as the three new CEOs that BP has had so not nearly the same upheaval. But following the proxy contest loss, Exxon’s incumbent directors (again, among many, many other differences) potentially benefited from the tenure and institutional knowledge to absorb the insurgents: lead independent director Kenneth Frazier was twelve years into his service, Ursula Burns almost nine, and CEO-chairman Woods five and counting. (Not every veteran survived the vote: Samuel Palmisano, fifteen years a director, was one of the three incumbents — alongside Douglas Oberhelman and Wan Zulkiflee — who lost their seats to the dissidents.) The new directors were integrated into a functioning power structure with settled views on strategy. There were no walkouts, no leaks, no factions. Hietala and Karsner remain on the board today, while Exxon doubled down on oil through the Pioneer acquisition. The activists changed the composition of the board, but not how the company was run.

BP’s board, by contrast, seemingly had no one with the standing to manage either Elliott or the chair Elliott favored. The directors evaluating Manifold’s appointment had a median tenure of roughly three years; several had never sat through a full strategy cycle. A weak board acquiesced quickly to a strong-willed chair — then discovered, within months, that it had the wrong one, and needed a public defenestration to correct course. Both decisions may individually have been defensible, but the whiplash has left investors unsettled.

Shareholders have noticed the difference: Exxon’s five-year total return of roughly 193% comfortably outruns BP’s 149%, most of the gap opening after BP’s strategy began wobbling in 2023–2024. BP shares have rallied significantly in 2026 — up 37% year to date — though how much of that reflects confidence in the new team versus speculation that someone else will end up running the company entirely.

Not too long and not too short

There are very good reasons to question a director’s independence after 9 years. So maybe the question is if (a little) less independence is worth taking the time to justify some directors sticking around longer. The U.K. Code permits explanation over compliance, and Provision 19 explicitly allows a chair to stay past nine years to facilitate succession. The tools for keeping experience exist; U.K. boards and their shareholders have simply made using them socially awkward.

But BP’s last eighteen months are a fair test of what the trade buys. A board needs institutional memory most exactly when an activist arrives, a chair misfires, or a strategy reverses — the moments when knowing where the bodies are buried (and which strategies have already failed once) is worth more than a clean independence checklist. The question investors should consider is if a BP board with two or three Frazier-vintage directors would have chosen Manifold? Would it have needed to?

Long-term planning requires someone in the room who can remember the last long-term plan.

This post is provided for informational purposes only and does not constitute investment advice, financial guidance, or a recommendation regarding how to vote on any proxy proposal. While the analysis and figures presented are derived from public filings and company reports and are believed to be accurate at the time of publication, they are provided without guarantee or warranty. Readers should conduct their own independent research and consult with a qualified professional before making any financial or voting decisions.

About Canbury

Canbury Insights is a technology-enabled sustainability consultancy applying AI tools to thoroughly and cost-efficiently deliver sustainability projects. We combine global expertise and local delivery to support organisations across the world to find the value in sustainability.

Copyright © 2026, Canbury Insights Limited. All rights reserved.