Bringing a Nuke to a Data Center Proxy Fight

Fermi America’s board battle, AI-adjacent investing challenges, and evaluating director skills for different goals

Riding the AI infrastructure boom has proven more challenging than expected for Fermi America and may offer a parable for other AI-adjacent players. Fermi’s stock is down approximately 60% since its IPO last October as its anchor tenant failed to materialize for its planned massive data center and private grid.

The AI infrastructure buildout is one of the most powerful investment themes currently. Data centers require enormous, reliable power, and the public grid cannot deliver it on AI timelines. Fermi America assembled permits, land, pipeline rights, turbine equipment, and nearly $1 billion in financing with impressive speed to capture this opportunity. The team that has taken over may yet prove the thesis right, but the stock’s trajectory from $21 to under $9 underscores the challenge. And as Oracle’s shareholders learned again this week, even the market narrative has limits.

The company’s founder and CEO, Toby Neugebauer, was terminated for cause in April. Now he is soliciting shareholders to call a special meeting, expand the board by seven seats, and install a new director slate with a mandate to pursue an immediate sale of the company he built.

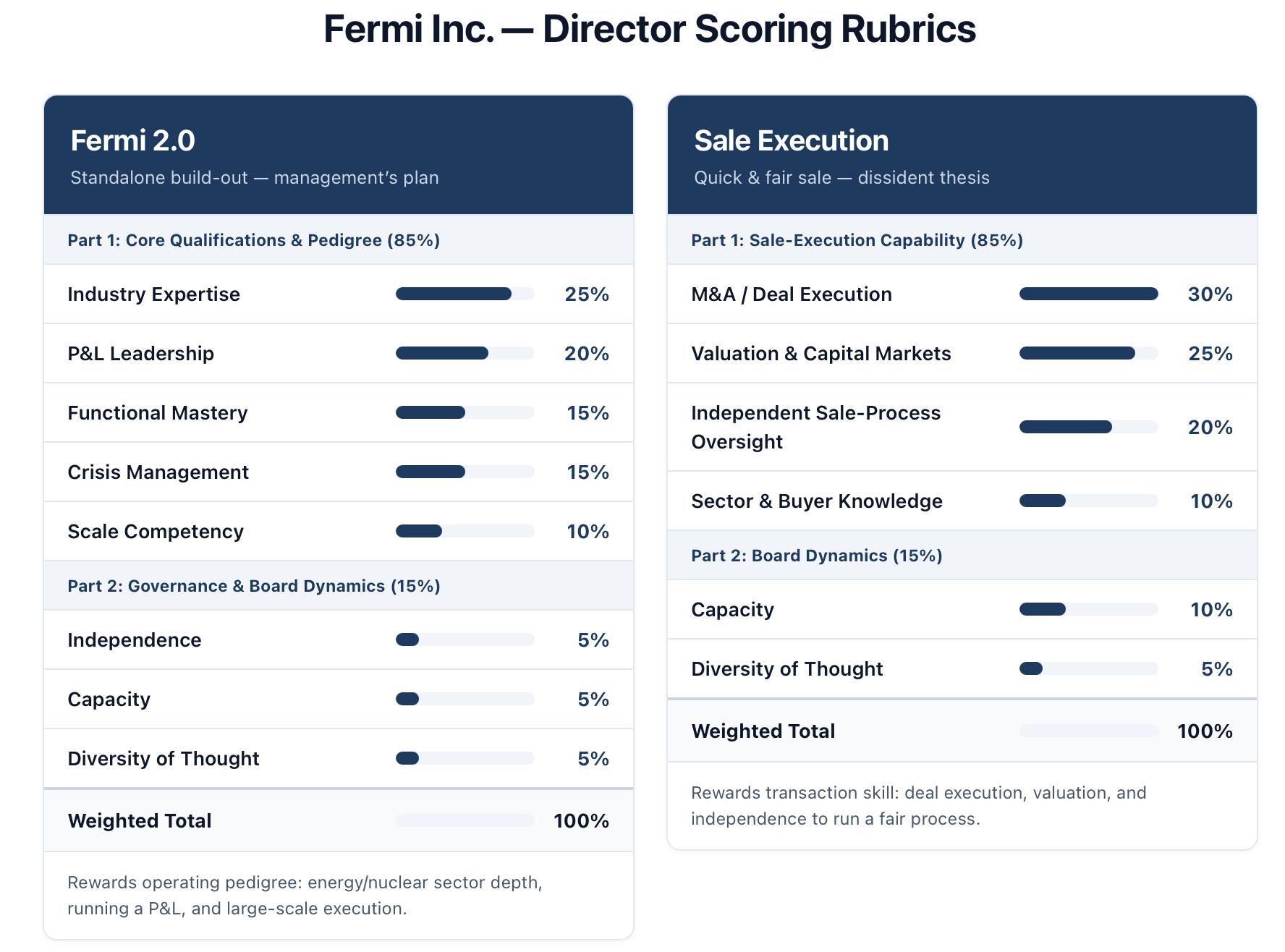

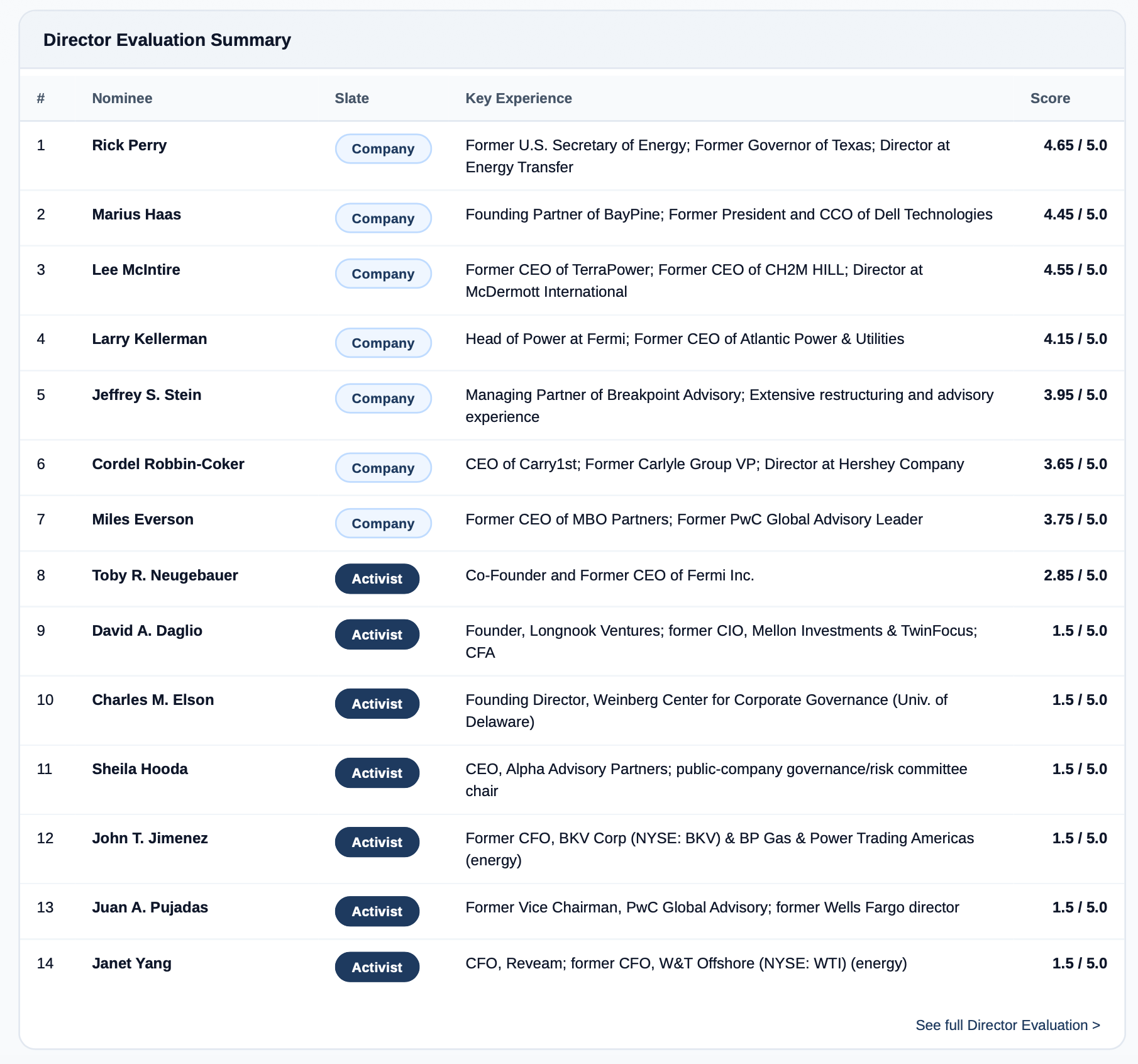

As in many proxy fights, there is a tension between management’s long-term strategy succeeding and an activist’s push for quick, short-term returns. Running the contest materials through Canbury’s ProxyPro platform using different investor personas, the director skill sets tell a divided story: Fermi’s current board is well-configured to build, permit, and operate a massive power infrastructure campus; the seven nominees Neugebauer has assembled are financial and governance specialists more naturally suited to orchestrating a sale.

The Contest: Builder vs. Seller

Fermi’s mission is to build Project Matador, a roughly 7,500-acre data center campus and 17-gigawatt private power grid run on natural gas and a newly built nuclear reactor in Amarillo, Texas. The pitch of reliable, lower carbon power appeals to the investor enthusiasm for AI infrastructure, but the execution ran into the core challenge in real estate development: you need tenants.

Neugebauer co-founded Fermi Inc. in January 2025, went public in October at $21 per share, assembled permits, land rights, gas pipeline access, and turbine equipment in record time, and then failed to sign a tenant. The stock cratered in December after the planned anchor tenant never followed through on its letter of intent. After being terminated for cause on April 30, 2026 (the board citing misrepresentations, policy violations, unauthorized meetings, and threatening behavior toward staff and counterparties), Neugebauer launched a consent solicitation to call a special meeting of shareholders, targeted for approximately July 15, 2026.

His proposals: repeal bylaw amendments the board adopted after his removal (including a measure raising the threshold to amend board size to 70%, which management calls a governance protection and Neugebauer calls the “Insiders Veto Amendment”), expand the board by seven seats, elect seven nominees, and remove three sitting directors for cause. The stated goal is to install a board that will pursue an immediate sale.

Fermi’s current leadership—operating under the “Fermi 2.0” banner with co-presidents Anna Bofa and Jacobo Ortiz—counters that commercial discussions with potential tenants are at a “critical juncture,” that the company is in discussions with seven potential tenants and twelve potential joint venture partners, and that an immediate sale at current prices would transfer value built by public shareholders to Neugebauer, who acquired his founder’s equity at approximately $0.0067 per share versus the $21 IPO price, and the current share price of $8.66 as of June 17 close.

For shareholders, supporting a vote for a special meeting, and then proposed governance and board changes comes down to their views of how to proceed. To evaluate the two slates of directors, we consider the necessary skill alignment and evaluation scoring rubric for the two different strategies. We then apply ProxyPro’s AI-powered tools to evaluate each director against the criteria.

Obviously one can have different views on the correct criteria, and all of the sub-criteria we have behind these criteria, along with their weightings. The point is not to provide a definitive answer, but to demonstrate the ability to use AI tools to quickly run different, subjective assessments across not just one proxy contest, but any contest.

What Fermi’s Strategy Requires from Its Board

Fermi America is a capital-intensive energy infrastructure developer claiming to have assembled the physical, regulatory, and financial foundation for the world’s largest private AI power campus. The “Fermi 2.0” strategic plan requires securing hyperscale data center tenants, delivering first generation capacity (200 MW) by Q4 2026, scaling to 1,458 MW by Q4 2027, advancing a nuclear combined operating license application with the Nuclear Regulatory Commission (the first accepted filing in 15 years), managing Department of Energy financing processes, and maintaining REIT structure compliance.

The company’s current directors are well-aligned for the hard work of Fermi 2.0: permitting, construction, power generation, regulatory navigation, and tenant development. The deficiency is on the financial governance and M&A oversight side, which becomes material if strategic alternatives are ever formally considered. Neugebauer’s activist slate is not.

Fermi 2.0 director skill alignment

The Directors to Lead a Sales Process

Alternatively, if shareholders think that it’s actually not so easy to build a data center and power infrastructure from scratch and finding a respectable exit is best, the director evaluation looks different.

Sales execution director skill alignment

It is worth calling out that even through this “sales execution” lens, two of the current (management) directors score best and the dissident activist directors rank in a wide range.

The AI-Adjacent Investment Parable

Fermi’s stock trajectory reflects a pattern in the AI hype cycle. After rising more than 50% in the days following its $21 IPO, shares cratered when the anchor tenant failed to materialize. They have since bounced—rising sharply on the Fermi 2.0 announcement and jumping more than 22% in a single session last week after an analyst suggested OpenAI may be evaluating capacity at Project Matador—yet still trade roughly 60% below the IPO price.

Similarly, consider Oracle. On September 10, 2025 (shortly before the Fermi IPO), the company reported blowout earnings and a contracted AI cloud backlog that would eventually swell past $638 billion. Its stock hit an intraday high of $345.72, closing at $328.33. The market was pricing Oracle as a primary beneficiary of the AI infrastructure boom.

By April 9, 2026, the stock had fallen to $138, a decline of 58% from that September close, 60% from the intraday peak. Investors had grown concerned about the capital intensity required to sustain the AI cloud buildout. Then, on June 11 of this week, Oracle reported Q4 results showing annual capital expenditures of $55.7 billion—above the company’s own $50 billion forecast—and guided to $95 billion in CapEx for fiscal 2027. The stock fell 8.5% the next session. Oracle has since partially recovered to $188.33, but sits over 40% below its September peak.

There are clearly big differences between Fermi and Oracle, not least of which Oracle’s $67 billion in annual revenue and $638 billion contracted backlog compared to Fermi’s zero revenue from operations and no signed tenant. Fermi faces similar skepticism as Oracle, but none of its cushion to absorb it.

Fermi’s proxy contest crystallizes the investor’s choice: a board configured to build a gigawatt-scale power campus, or a board configured to sell the asset while there is still a willing buyer.

This post is provided for informational purposes only and does not constitute investment advice, financial guidance, or a recommendation regarding how to vote on any proxy proposal. While the analysis and figures presented are derived from public SEC filings and company reports and are believed to be accurate at the time of publication, they are provided without guarantee or warranty. Readers should conduct their own independent research and consult with a qualified professional before making any financial or voting decisions.

About Canbury

Canbury is a technology-enabled sustainability consultancy applying AI tools to thoroughly and cost-efficiently deliver sustainability projects. We combine global expertise and local delivery to support organisations across the world to find the value in sustainability.

Copyright © 2026, Canbury Insights Limited. All rights reserved.