Six Flags Over Texas

Exxon, ArcBest and Evaluating Shareholder Protections in Texas Redomicile Proposals

Companies are leaving the shareholder-aligned—or at least well-defined—confines of Delaware for the corporate-friendly open plains of Texas. Recent reforms to the Texas Business Organizations Code (TBOC), along with the 2024 launch of the specialized Texas Business Court, have attracted a wave of companies to propose redomiciling in the Lone Star State. The concern among institutional investors is what rights are they losing to hold boards accountable in the Texas shuffle.

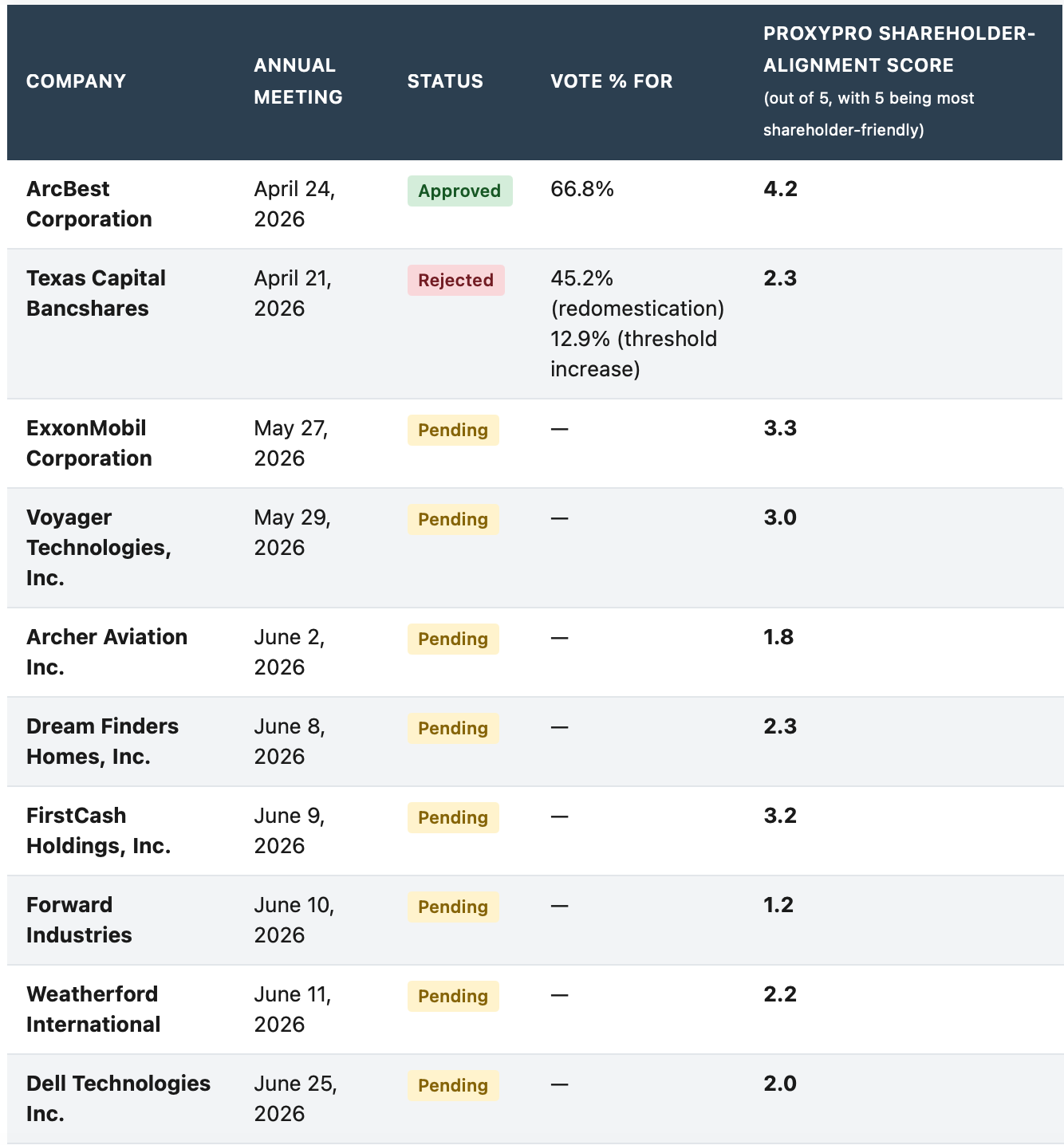

ArcBest saw two-thirds shareholder approval for its redomicile proposal in April, while Texas Capital Bancshares narrowly experienced defeat. ExxonMobil has its proposal going to a shareholder vote later this month, along with a number of other companies this season, including Dell Technologies.

Taking a page from Six Flags amusement park - named after the six sovereign flags that have flown over Texas - Canbury Insights’ ProxyPro platform uses a six-flag assessment for scoring companies on their redomicile proposals. The ride can be thrilling or terrifying, depending on where you are sitting.

Please note that this is absolutely, positively not voting advice, nor investment advice, but definitely not voting advice. You read beyond this point at your own risk and with clear understanding that this is not voting advice.

Great Adventure

Texas is making a play for the incorporation game that has been a Delaware specialty because of its 100+ years of corporate case law, giving boards, shareholders, and their lawyers a reliable rulebook. The TBOC reforms and the Texas Business Court have been engineered to attract companies with two key selling points: efficiency (specialized judges, faster dispute resolution, published opinions) and insulation (shareholder litigation is harder, more expensive, and more likely to favor the board).

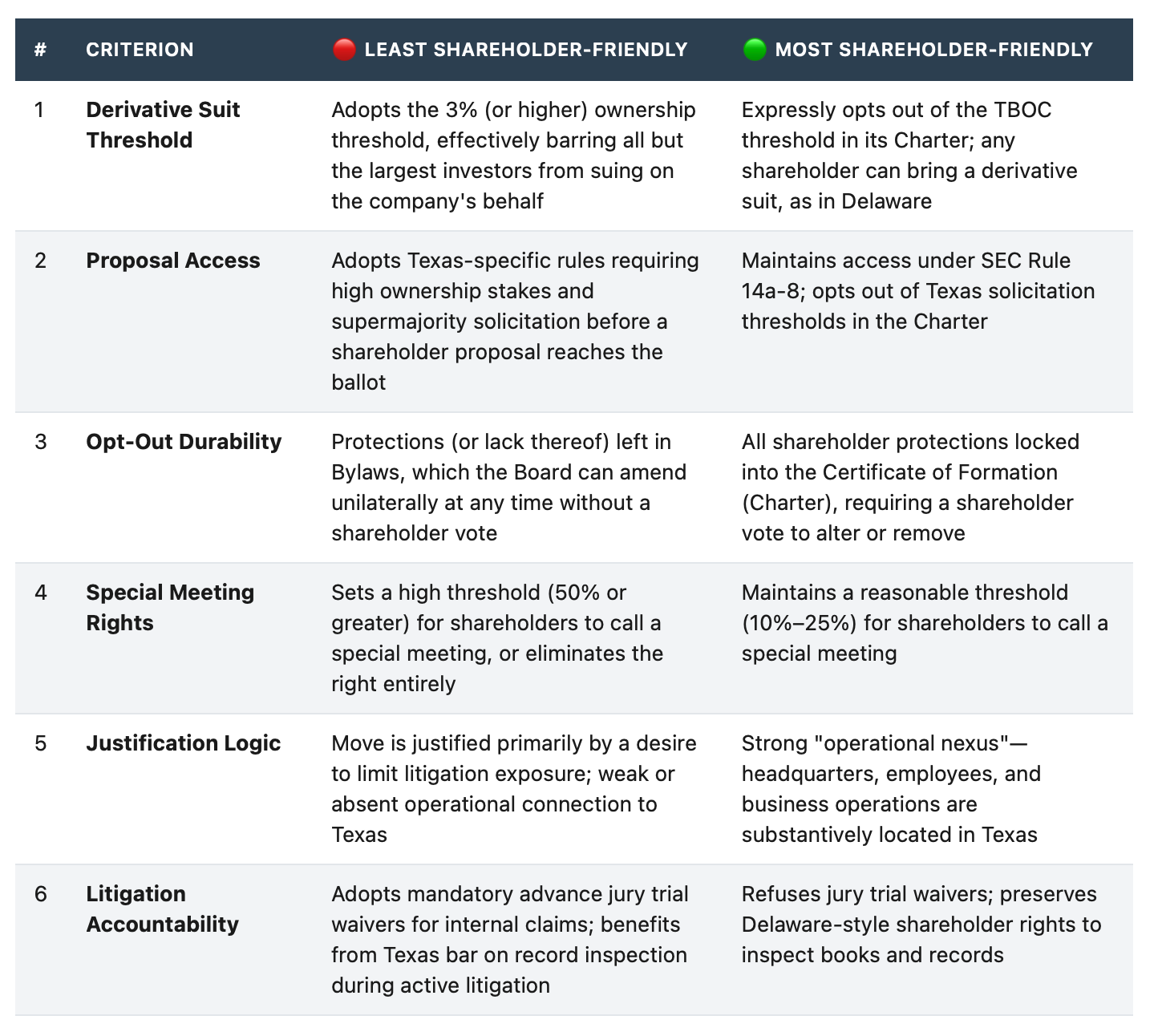

Key issues for investors to consider in a Texas re-domicile proposal:

Restrictive Shareholder Proposal Access. TBOC Section 21.373 allows companies to require that a shareholder own 3% of shares and solicit 67% of the voter base before a proposal can even appear on the ballot. That is an extremely high threshold.

The “3% Rule” for Derivative Suits. Texas now permits companies to block any shareholder from suing on the company’s behalf unless they own at least 3% of outstanding shares. At ExxonMobil’s market cap, that represents roughly $19 billion.

Jury Trial Waivers. Texas governing documents can require that internal corporate disputes—fiduciary duty claims, derivative suits—be decided by a judge alone, not a jury. Bench trials in a court whose judges are appointed by the Governor on two-year terms represent a material shift in the litigation landscape.

The Charter Gap. Perhaps most importantly, many companies are making commitments not to adopt some of these shields in their proxy disclosures, while simultaneously refusing to write those commitments into their Charters. A Board policy is just a policy that can be changed anytime. A Charter provision requires a shareholder vote to change.

ProxyPro’s Six Flag’s Framework

Canbury Insights’ ProxyPro assesses Texas redomicile proposals across six criteria, each scored from 1 (Management Entrenchment) to 5 (Shareholder Friendly). We run the framework with our AI-powered tools, which allows us to surface the specific governance choices companies make — and helps investors to make informed decisions. Each criteria is equally weighted, which reasonable people can disagree with. And, to reiterate, we do not recommend how to vote.

Equities in Dallas

The table below highlights some of the recent and upcoming Texas redomicile proposals up for a vote and our rules-based, transparent scoring based on public disclosures.

Company Deep Dives

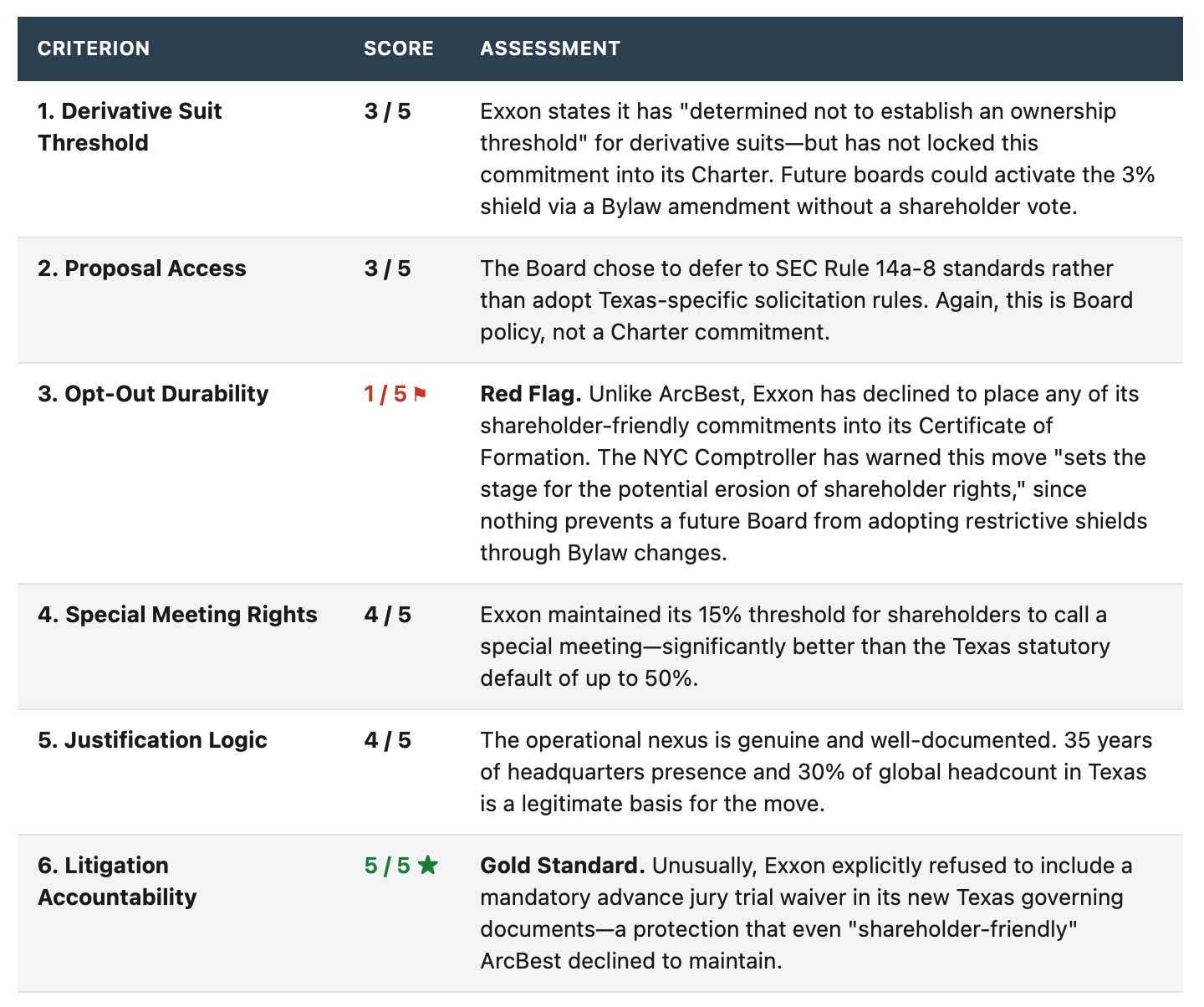

ExxonMobil Corporation — Score: 3.3 / 5.0

Proposal Vote: May 27, 2026

ExxonMobil’s redomicile from New Jersey—its legal home for over a century—to Texas is the highest-profile move of the 2026 proxy season. The operational case is clear: Exxon’s global headquarters has been in Texas for 35 years, and roughly 30% of its global workforce is based there. The governance story is more complicated.

The Exxon proposal scores strongly in some areas and lower in others on shareholder alignment. An additional concern: Exxon is simultaneously rolling out a Voluntary Retail Voting Program that allows retail shareholders to give standing instructions to vote in lockstep with Board recommendations. With retail investors owning approximately 38% of the company, critics have warned this creates a structural advantage for management on close votes—including this one.

The New York City Comptroller has come out against the proposal, specifically on the Charter lock issue. That opposition, combined with the retail voting program, makes the May 27 vote one of the more closely watched governance contests of the season.

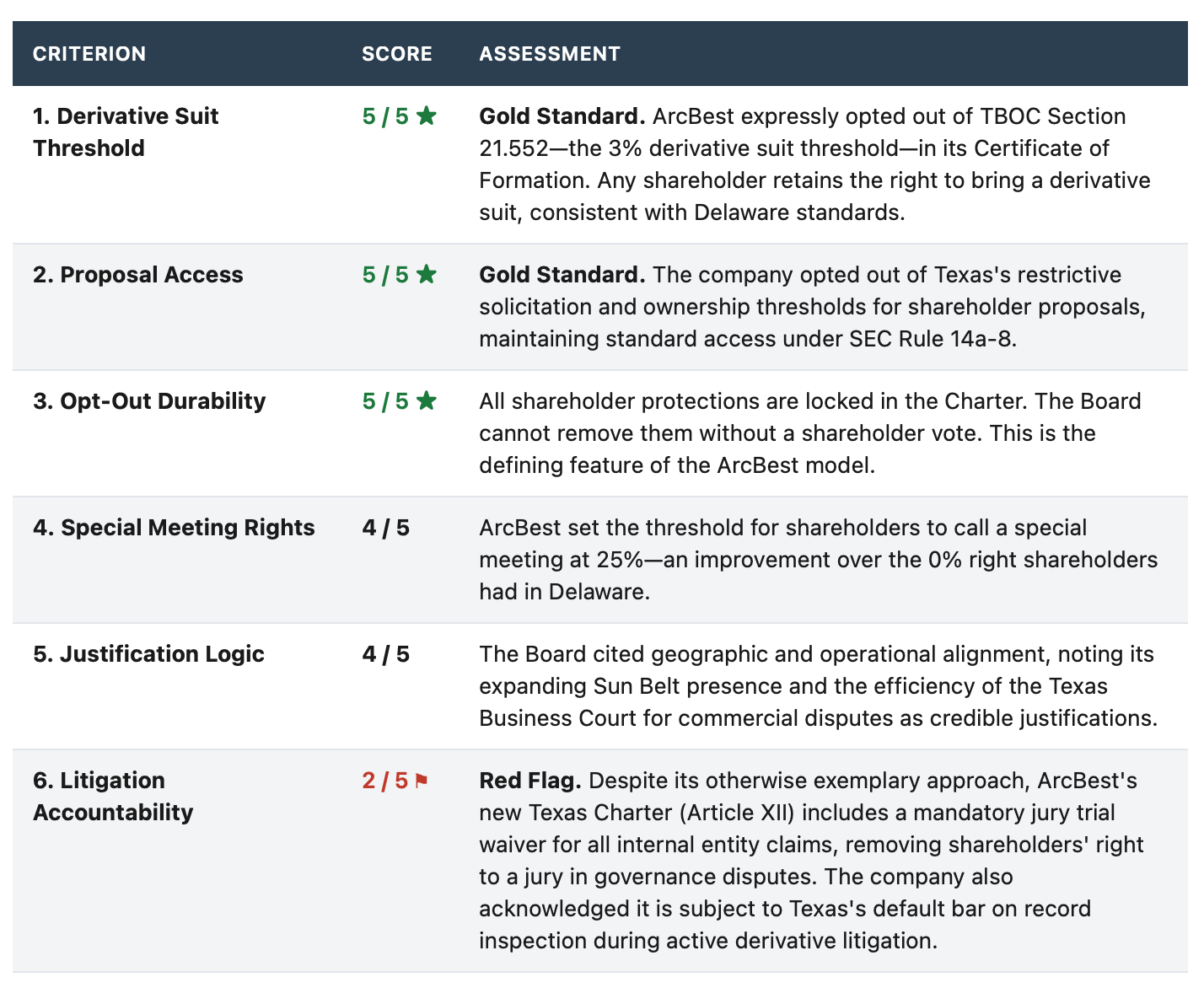

ArcBest Corporation — Score: 4.2 / 5.0

Proposal Vote: April 24, 2026 — Approved, 66.8%

ArcBest’s redomicile is seen by some as a template for how to move to Texas without betraying your shareholders. The Fort Smith, Arkansas-based freight and logistics company chose to write its shareholder protections directly into its new Texas Charter—not just its Bylaws—making them permanent absent a future shareholder vote. Even still, one-third of shareholders voted against the proposal showing a fair share of unease with the move.

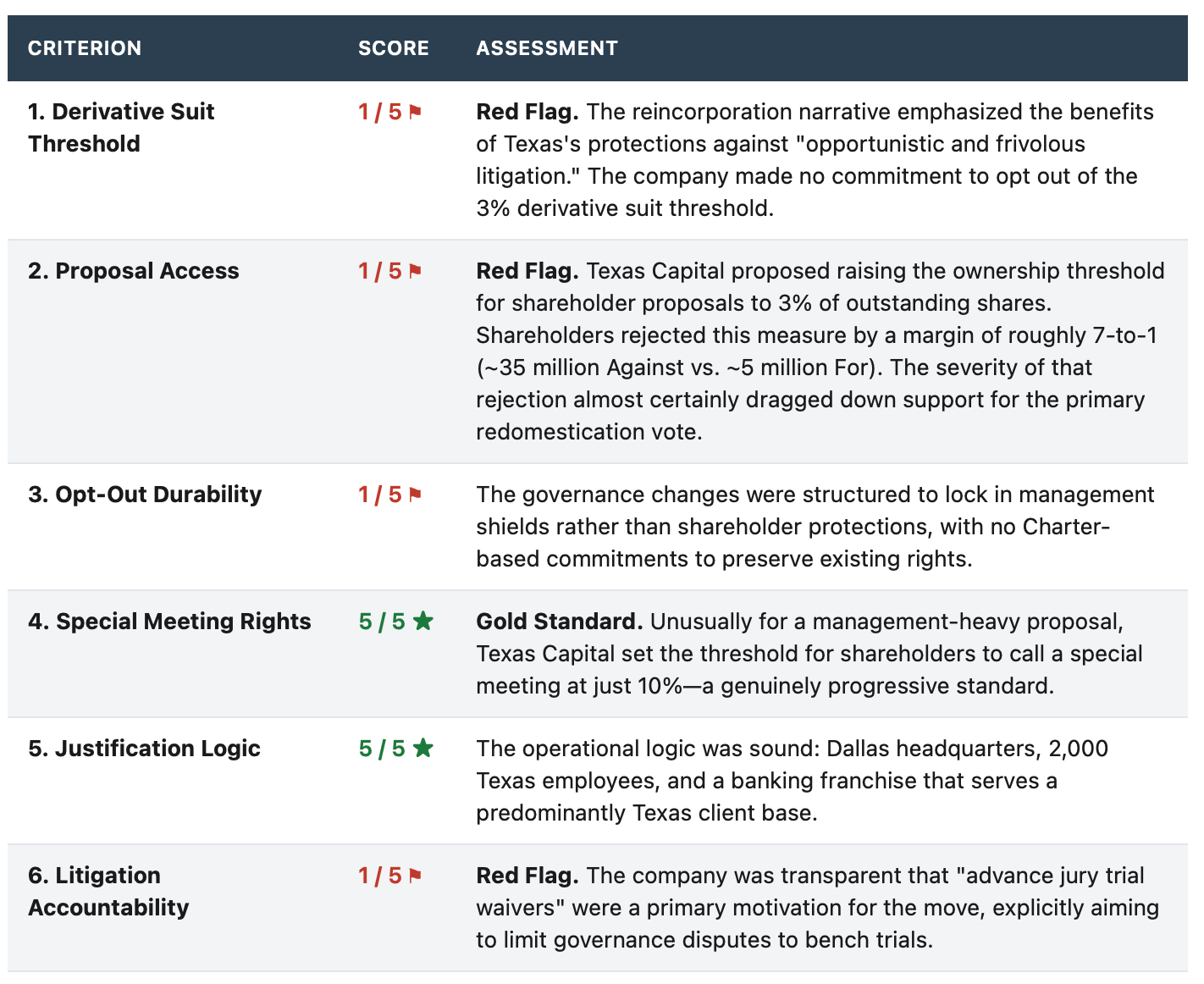

Texas Capital Bancshares — Score: 2.3 / 5.0

Proposal Vote: April 21, 2026 — Rejected, 45.2% Approval

Texas Capital Bancshares provides a cautionary tale. The Dallas-based bank had a reasonable operational case for the move—2,000 employees in Texas, headquarters in Dallas, and a business that is fundamentally Texan in character. What it did not have was a proposal that shareholders were willing to accept.

Looking ahead, Exxon’s proposal sits in-between the ArcBest approach approved by shareholders and the Texas Capital one that was not. The vote will likely come down to investors’ views on how much they are giving up and how much goodwill its board has earned with investors.

Canbury Insights’ ProxyPro is a governance analytics platform for institutional investors and corporate governance professionals. This post is provided for informational purposes only and does not constitute investment advice, financial guidance, or a recommendation regarding how to vote on any proxy proposal. While the analysis and figures presented are derived from public SEC filings and company reports and are believed to be accurate at the time of publication, they are provided without guarantee or warranty. Readers should conduct their own independent research and consult with a qualified professional before making any financial or voting decisions.